« October 10, 2008 |

Main

| October 12, 2008 »

Saturday, October 11, 2008

Gnome-o-gram: Deleveraging—It's All About the Debt

You could read almost all of the voluminous coverage of the present crisis in the financial markets in the legacy media without ever encountering the essential term which describes what's going on at the “big picture” level, understanding the underlying cause for the events in the news, or comprehending the magnitude of the problem and how protracted may be its consequences.

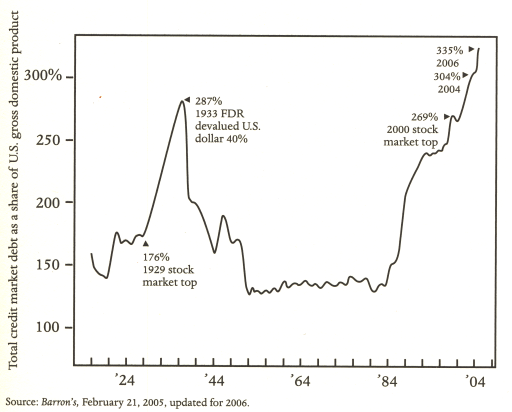

The following chart, from p. 7 of Kevin Phillips's

Bad Money, encapsulates everything you need to know about the present situation. This is not a “mortgage crisis”, “derivatives crisis”, “credit crisis”, or any of the other terms bandied about describing aspects of the larger situation—it is a

debt crisis and it always has been. The United States have experienced a multi-decade bubble market, rolling over from equities and real estate in the 1980s, to technology stocks in the 1990s, and back to residential real estate in the aughties, all driven by an unprecedented explosion of debt, as illustrated below.

The chart shows total debt in the United States, both public and private, as a fraction of the U.S. Gross Domestic Product (GDP). Over much of the last century, during both periods of robust growth and recession, total debt has averaged around 150% of GDP, but there have been two periods, in the boom leading up to the 1929 crash and the subsequent depression, and starting around 1984, when debt has exploded with respect to GDP, in the present epoch rising almost vertically into unexplored territory. This chart covers only the period ending in 2006; since then the near-vertical rise has continued, reaching a level of 349.5% of GDP at the end of March, 2008—here is a

proprietary chart showing the recent evolution of this measure.

At the root of every financial bubble is

leverage: the ability through debt or other financial instruments, to increase the buying power of those bidding up prices based upon the apparently appreciating values of the asset at the centre of the bubble. Although human creativity is unlimited, especially in the domain of financial fantasy, the leverage in most bubbles ultimately comes down to debt, and that is certainly the case at present. Politicians and the legacy media are constantly prattling about the national debt and the trade deficit, but these are small potatoes compared the the explosion of private debt, primarily in the financial, business, and household sectors which has occurred in recent decades. For example, between 1994 and 2006, the U.S. federal government debt increased from 3.5 to 4.9 trillion dollars—far from pocket change, to be sure, unless you have

really deep, Uncle Sam sized pockets—but domestic financial sector debt grew from 3.8 to 14.2 trillion dollars, other business debt from 3.8 to 9.0 trillion, and household (mortgage, credit card, and installment purchase) debt from 4.5 to 12.9 trillion. Thus, despite the media focus on public debt, it is an almost negligible component in an explosion of debt almost entirely in the private sector, which has fueled a bubble market in the assets into which this money, created more or less out of thin air, has flowed.

For all of the talk about derivatives, mortgage-based securities, credit default swaps, and all of the other financial arcana created by backroom string theorists who didn't get tenure and had to shift their career goals from

destroying theoretical physics to wrecking the global financial system, most of these instruments are ultimately ways to repackage

debt, financial alchemy transforming leaden debt into golden AA/AAA rated securities, at least until a

black swan lands on your pond, its ripples bringing the entire fairy castle down.

And so,

it's all about the debt: a collapsing bubble built upon debt created based on asset values inflated by earlier debt, and around and around we go, until the music stops. Music? I don't hear it any more. We're looking, as we did in the 1930s, at the liquidation of a massive stock of debt, unprecedented in its size in human history, which any dispassionate observer would immediately conclude cannot be repaid, or if repaid, only at a steep discount to its face value. This

deleveraging (another term you may have first encountered here, but you're sure to hear innumerable times in the legacy media chatter in the next several months) is just in its early stages at present. Any number of things could have triggered it: in this case it was the subprime mortgage collapse, but it could equally have been a run on the dollar, a Chinese move out of U.S. Treasury securities, OPEC repricing oil in Euros, or any number of other proximate causes. The underlying situation is the debt bubble, and its deflation will be the main story of what happens hence.

How bad is it going to be? Well, just keep your eye on that total debt versus GDP number. It usually runs around 150%, and at present it's at 350%. The fact is, most of the assets which secure that debt are themselves inflated by the bubble, to the extent that nobody knows what they're really worth. But if you imagine the debt bubble deflating to its historical value, then you're looking at a fall of more than 50% in asset values blown up in the bubble. In historical terms, this is typical. If you're a homeowner leveraged to the hilt with equity loans, it may be tragic.

Let's cut to the essentials. Much of that debt written in the last few years has been granted to borrowers who

can't pay it back. The assets which supposedly secured the debt were themselves inflated by the bubble created by earlier debt, and now have a market value below that of the principal of the loan. Such a situation will ultimately end in “debt liquidation” or “deleveraging”—the evaporation of debt-created wealth as borrowers default upon their obligations. What does this mean for the economy? Remember that every borrower's debt is a creditor's asset. When a borrower defaults, the creditor sees their asset evaporate, and that's how that first spike we see in the chart above came back down to reality in the 1930s. And because the market for debt-based securities is global, the excesses of the U.S. credit market will afflict financial institutions worldwide who were so imprudent as to buy them based on credit ratings computed by

manqué string theorists.

Note that “bailouts” as presently proposed and implemented make

no difference whatsoever in this chart. They're just a transfer of debt from the private account to the public account. While this may make a big difference to creditors of the rescued companies and to the taxpayers put on the hook to assume the consequences of speculative mismanagement, it doesn't make a whit of difference to the aggregated debt picture: somebody's going to have to pay back that Mount Everest of debt, or else default on it, or (the way to bet, once it's assumed by the government) inflate it away.

Other gnome-o-grams

Posted at

19:55